How to Review Recurring Charges Without Connecting Your Bank Account

Learn a simple, privacy-friendly way to review recurring charges using statement uploads and transaction cleanup, so your household can spot waste without bank sync.

How to Review Recurring Charges Without Connecting Your Bank Account

You do not need bank sync to find subscriptions, repeating bills, and quiet monthly leaks.

Why this matters

Many households want a clearer view of recurring charges, but not everyone wants to connect bank accounts to another app. Sometimes the concern is privacy. Sometimes it is reliability. Sometimes it is just a preference for slower, more deliberate money management.

That does not mean you have to guess where your monthly money is going. With a few recent statements, clean transaction names, and a simple review routine, you can still find streaming services, app renewals, duplicate memberships, and forgotten annual charges. A no-bank-sync workflow can be calm, private, and surprisingly effective.

What this means in real life

A real household usually does not have one neat list of subscriptions. One parent signs up for a kids' app. Another starts a music subscription. A gym charge keeps going after attendance drops. None of this looks dramatic on its own, but together it can turn into a steady monthly drag.

The problem is rarely that people are careless. The problem is that recurring charges hide when merchant names are messy or dates shift slightly. A good review process is not about guilt—it is about visibility.

Step 1: Gather three months of statements

What to do

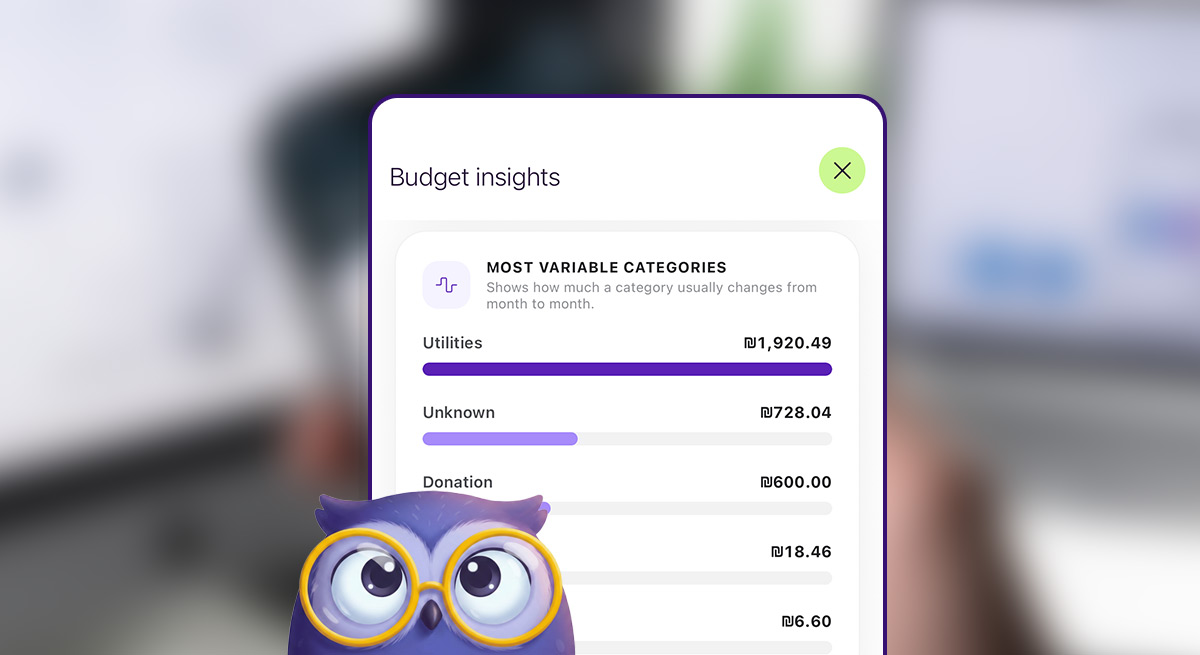

Start with the last three months of card or bank statements you actually use for household spending. If you use aynWise, you can upload statements to keep the process contained in one place.

Why it helps

Three months is the "sweet spot" to catch monthly subscriptions, recurring service bills, regular school fees, and recent price changes. It helps you distinguish a true recurring charge from a one-time purchase.

Common mistake to avoid

Do not start with a full year if you are already overwhelmed. Three months is usually enough to get traction without the burnout.

Step 2: Clean up transaction names

What to do

Normalize merchant names so repeats are obvious. For example, "SPOTIFY 2F4K3" and "Spotify SE" should both be labeled simply as "Spotify." Clean transaction names in the transactions page to make your list readable by a human, not a bank computer.

Why it helps

Recurring charges hide inside inconsistent labels. Once names are cleaned up, patterns appear instantly: the same merchant every month, similar amounts on a regular schedule, or multiple charges from related services.

Common mistake to avoid

Do not cancel things before you are sure what they are. First make the data readable, then decide what stays and what goes.

Step 3: Separate essential repeats from quiet extras

What to do

Mark repeating charges in two groups:

- Expected household essentials (Electricity, insurance, school payments).

- Optional or review-needed items (Streaming, storage upgrades, trial conversions).

Why it helps

Not every recurring charge is a problem. The goal is to know what still earns its place in your monthly spending. This makes household conversations easier; instead of saying "we spend too much," you can say, "we have three services no one is using."

Common mistake to avoid

Do not treat all recurring charges as equal. A necessary utility bill and an unused app subscription deserve very different decisions.

A simple example

A household reviews three months of statements and finds a $10.99 music sub, $9.99 cloud storage, and a $24.00 old fitness plan. After cleaning up the names, they realize they have two different cloud storage accounts for the same purpose. They cancel the unused fitness plan and the duplicate storage, saving nearly $35 a month—no bank sync required.

Signs your current approach is not working

- You notice charges only when the monthly total feels unusually high.

- Merchant names are so messy that you cannot tell what repeats.

- You are paying for at least one service no one in the household actively uses.

- You avoid reviewing subscriptions because the process feels annoying or unclear.

A better way to keep it manageable

The easiest recurring-charge system is the one your household will actually repeat. A privacy-friendly workflow where you upload statements allows you to stay in control of what data you share and when.

If you want a lighter way to do this, explore how to review spending patterns or check out the pricing page for a setup that fits your rhythm.

Frequently asked questions

Can I find recurring charges without linking my bank account?

Yes. Uploaded statements are often enough. Once transaction names are cleaned up, recurring charges usually become much easier to spot across a two or three-month window.

How many months should I review?

Three months is a strong starting point. It catches most monthly charges and gives you enough history to distinguish recurring payments from one-offs.

What should I do first if I find too many subscriptions?

Start by grouping them into essential and optional. Cancel the obvious non-used items first, then review the rest one by one.

Final thoughts

Recurring charges are hard because modern billing is designed to fade into the background. A simple review process brings those charges back into view. You just need readable transactions, a few recent statements, and a practical way to decide what still belongs in your household budget.

Related posts

The AI Advantage: Turning Your Bank Statement Into Clarity

Stop looking at rows. Start seeing your life. Learn how AI translates cryptic bank data into a story you can actually use.

How to Clean Up Unknown Transactions Before They Break Your Budget

A calm, practical system for turning unclear bank transaction names into categories you can actually use for household decisions.

The 10-Minute Weekly Financial Reset: A Guilt-Free Routine

Waiting until the end of the month to look at your finances is a recipe for stress. Keep your budget on track with a micro-routine that takes less time than drinking your morning coffee.